Australia

Markets React To Australian Rate Hold Decision

RBA holds rates at 3.60% as XRE and AU10Y reflect inflation surprises and measured policy stance maintaining growth and market stability.

Australia

RBA holds rates at 3.60% as XRE and AU10Y reflect inflation surprises and measured policy stance maintaining growth and market stability.

India

India’s RBI defends the INR near 84 and stabilizes the 10-year G-sec yield at 7.38%, supporting NSEI equities and capital inflows while addressing twin deficits and inflation risks in 2025.

African Development Bank (AfDB)

AfDB launches new climate financing instruments (CAW) as Africa demands institutional capital for adaptation and mitigation; with sovereign spreads and private-capital flows in focus, the bank aims to muster US $4bn by end-2025 for green transition.

Global Markets

The U.S. dollar slides versus yen and euro, affecting Asian FX markets and export competitiveness, with implications for USD-denominated debt, KR:BOKR, ID:BI, and regional portfolio strategies through early 2026.

European Union (EU)

The euro’s slide and forecast decline to approximately 1.15 reflect Europe’s growth and policy divergence, creating heightened FX-risk for EUR-zone allocations and hedged strategies.

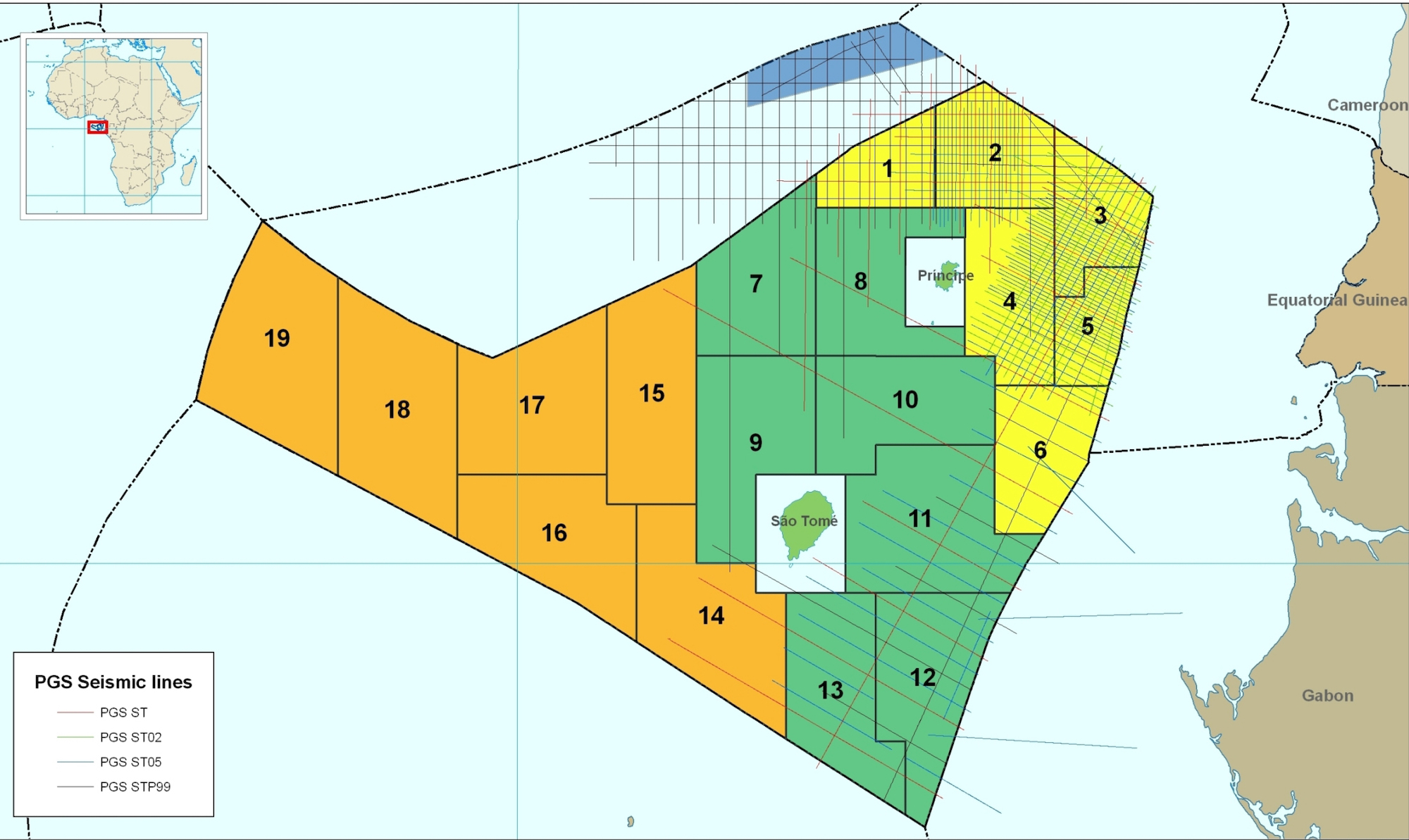

São Tomé and Príncipe

Shell begins drilling the Falcão-1 deepwater well in São Tomé’s Block 10, targeting pre-salt structures as Brent (CL=F) stabilises near US$85 and offshore momentum builds.

Indonesia

Rupiah opens at 16,620 per USD as DXY and CL=F remain strong; BI holds rate at 4.75%, reserves steady near $149b, and EMB reflects stable risk profile while JKSE shows resilience in a shifting regional market landscape.

Peru

Peru’s infrastructure push targets spread compression as PEN=X steadies near 3.40 and 10-year USD yields hover ~6.0%; credible execution offsets softer HG=F and supports a 2026–2027 growth lift with debt anchored near 31–33% of GDP.

Tanzania

Tanzania’s UDSM–industry collaboration aims to boost manufacturing productivity and exports as CPI stays near 3% and policy holds at 5.75%; monitor TZS=X and CL=F trends plus graduate employment data for execution credibility.

Rwanda

AI-enabled connectivity in Kigali signals a margin mix shift as $30–$40 devices expand usage; operators AAF.L and HTWS.L gain operating leverage while NVDA and MSFT monetise edge-cloud demand via AI infrastructure scaling.

Kenya

Record reserves lift buffers as KES=X steadies; new 7- and 12-year Eurobonds price below 9% and tighten spreads versus EMB while DXY strength and CL=F volatility frame external risks; watch CPI, USD/KES, and auction yields into Q4–Q1.

Côte d’Ivoire

Côte d’Ivoire’s push for local cocoa processing aims to lift manufacturing to 15 % of GDP and narrow its current-account deficit below 1 %, testing investor sentiment across CC=F, BARN.SW and EMB as policy execution defines spread direction.