Spreads vs. Sanctions: Will Liberia Trade Like SENEGL/IVYCST?

Liberia’s anti-corruption drive shows momentum—CPI 27/100, Afrobarometer approval 54%—but markets want follow-through. Track peer curves (GHANA 2032, NGERIA 2031, SENEGL 2033, IVYCST 2032) and sector catalysts (TotalEnergies LB-6/11/17/29). When cases mature, spreads compress—if institutions hold.

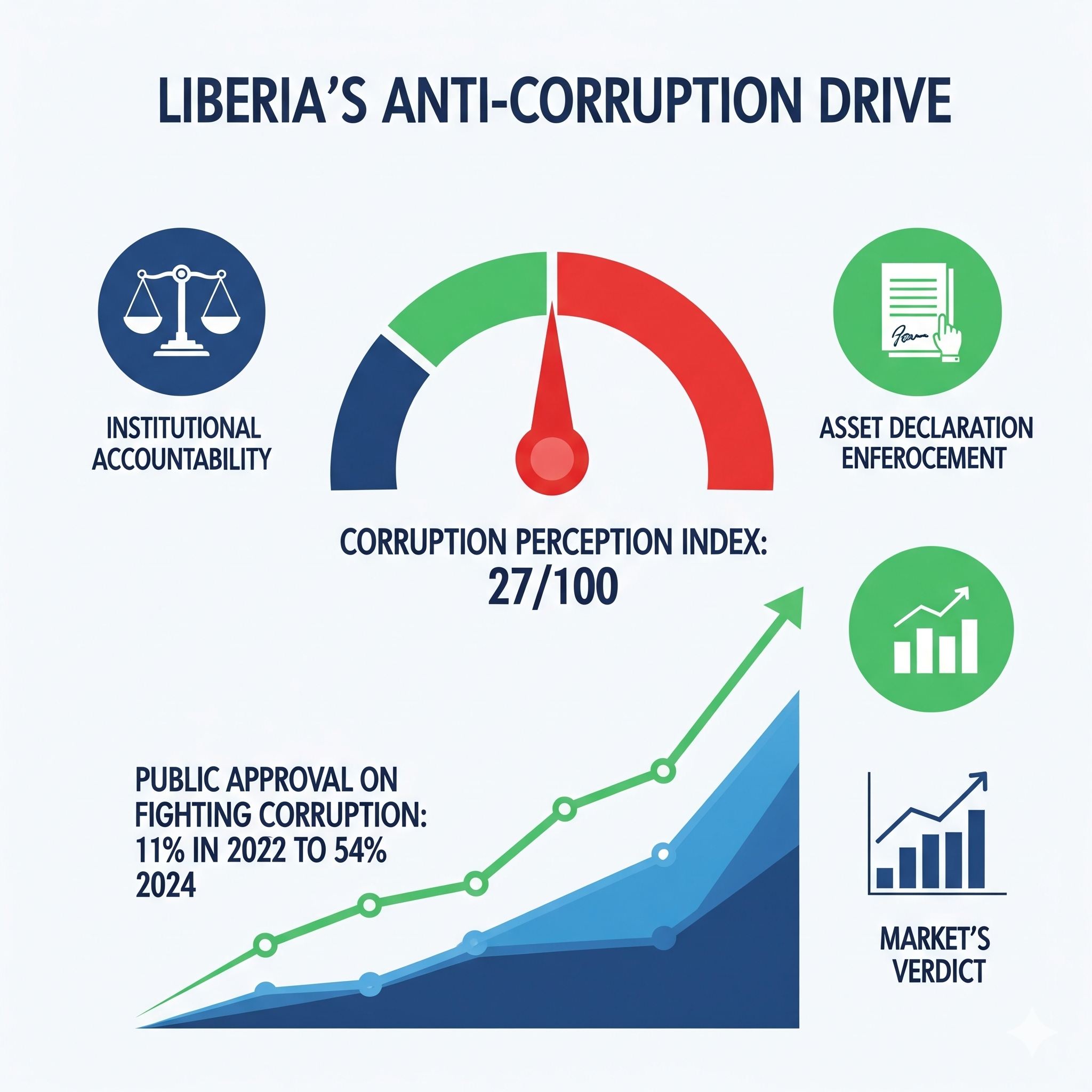

If Liberia wants markets to treat today’s anti-corruption drive as more than headlines, it has to show numbers that travel. On the governance side, the baseline is still low: Liberia’s CPI score is 27/100 for 2024—an improvement, but one that keeps the country deep in the global bottom quartile. That’s the “level.” The “direction” is stronger in public opinion: Afrobarometer reports a jump to 54% of citizens saying the government is doing fairly/very well fighting corruption, up 43 points since 2022, which signals political space for tougher enforcement and systems fixes. Markets will discount the optimism until the enforcement produces visible case maturation and recovered assets, but the swing in sentiment is a forward signal you can’t ignore.

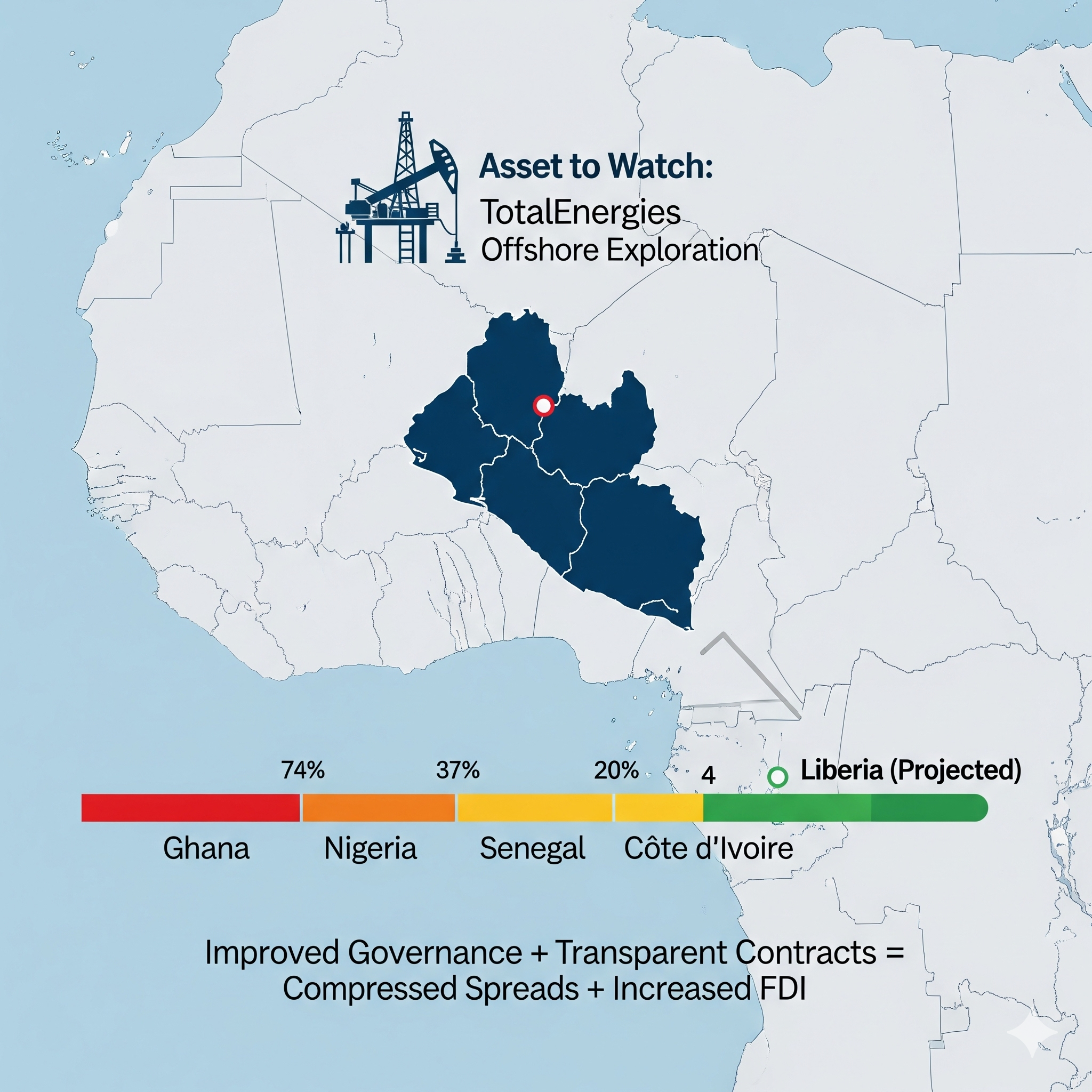

Because Liberia lacks a widely traded sovereign Eurobond curve, pricing the country’s governance risk relies on peer curves and sector catalysts. Start with ECOWAS benchmarks. For Ghana, the on-the-run hard-currency point is GHANA 8.125% 03/26/2032 (XS1968714540); for Nigeria, you can triangulate along NGERIA 8.747% 01/21/2031 (XS1910827887) and the DMO’s sheet of closes, where 2031s to 2051s were printing roughly 6.1%–9.2% YTM on 18 September 2025; for Senegal, SENEGL 6.25% 05/23/2033 (XS1619155564) is the staple; and for Côte d’Ivoire, IVYCST 4.875% 01/30/2032 (XS2264871828) anchors the top-tier WAEMU curve. The analytics move is to treat these as a regional control group: if Liberia’s governance actions are credible and its sector pipeline firms up, Liberia-exposed credits and FDI proxies should converge toward the “SENEGAL/IVYCST” end of the spread spectrum rather than the “GHANA post-restructure” end.

Sector news is the second leg of the analytics story. TotalEnergies just secured four offshore exploration permits covering blocks LB-6, LB-11, LB-17, and LB-29—12,700 km² in the southern basin—after a decade of limited interest. In a small, commodity-lean economy, even early-stage hydrocarbons optionality can change the shape of medium-term current-account expectations and sovereign risk premia—if licensing, local content, and revenue management are credibly governed. Analysts should therefore pair governance indicators with an asset-level tracker: award dates, work-program commitments, seismic progress, and any state-take disclosures. If the upstream timeline advances while CPI and WGI scores drift up, Liberia’s risk narrative shifts from “headline enforcement” to “enforcement + pipeline,” and peers will start to look like the proper valuation yardsticks rather than a courtesy comparison.

On policy momentum, two signals matter for the discount rate investors apply to Liberia: the breadth and depth of sanctions, and whether fiscal/monetary institutions are insulated as cases move forward. The past year saw the president suspend more than 450 officials over asset-declaration failures and even sideline the central bank governor after an audit flagged irregularities. For markets, those actions only compress perceived risk when they lead to charges, adjudication, and cash recoveries that reach Treasury—and when budget and central-bank operations stay orderly through the churn. That’s where IMF program anchoring helps: a live arrangement—even a modest one—gives investors a rules-of-the-road on fiscal and FX operations while the governance house-cleaning runs.

The practical analytics stack, then, is straightforward to implement in dashboards and notes without turning the article into formulas. Pin the governance baseline with CPI (score 27) and the latest Afrobarometer pulse; plot a peer-curve strip with GHANA 2032, NGERIA 2031/2034/2051 closes, SENEGL 2033, and IVYCST 2032; drop in a discrete event tracker for LB-6/11/17/29 milestones; and annotate each market move against policy steps like asset-declaration enforcement, prosecutions, and procurement digitization. If the next quarter brings case resolutions, visible upstream progress, and modest improvements in perception indices, expect Liberia-linked risk to begin shadowing SENEGL and IVYCST more closely than GHANA—and for local FDI proxies in telecoms, mining services, and logistics to reflect that convergence in deal terms and pipeline velocity.

The takeaway for a Pan-African audience is that Liberia’s governance story will be priced through peers and projects until it has its own liquid curve. That means the quickest route to cheaper capital is not only tougher enforcement at the top but also digitized procurement and transparent sector contracts that shrink discretion at the bottom. When sentiment, enforcement, and a tangible pipeline move together, spreads follow.