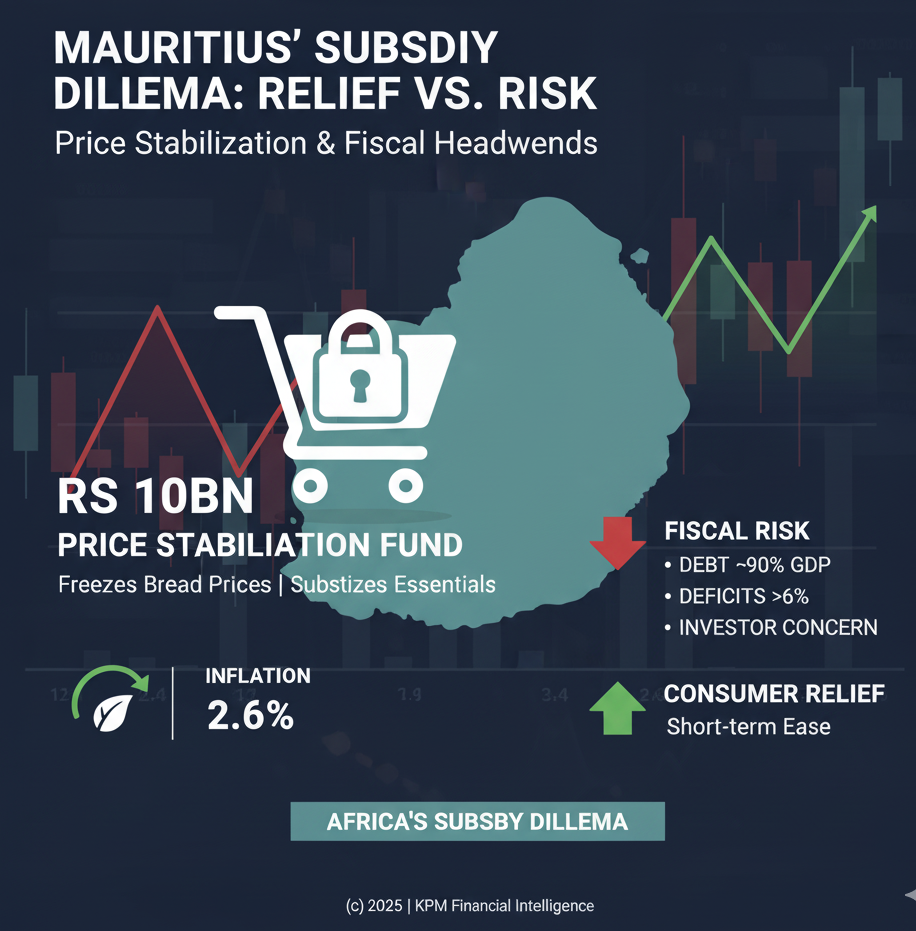

Mauritius’ Inflation Fight: Relief Today, Fiscal Questions Tomorrow

Mauritius’ Rs 10bn Price Stabilization Fund freezes bread prices and subsidizes essentials, easing inflation at 2.6%. But with debt near 90% of GDP and deficits above 6%, the move reflects Africa’s wider subsidy dilemma: relief today versus fiscal and investor risks tomorrow.

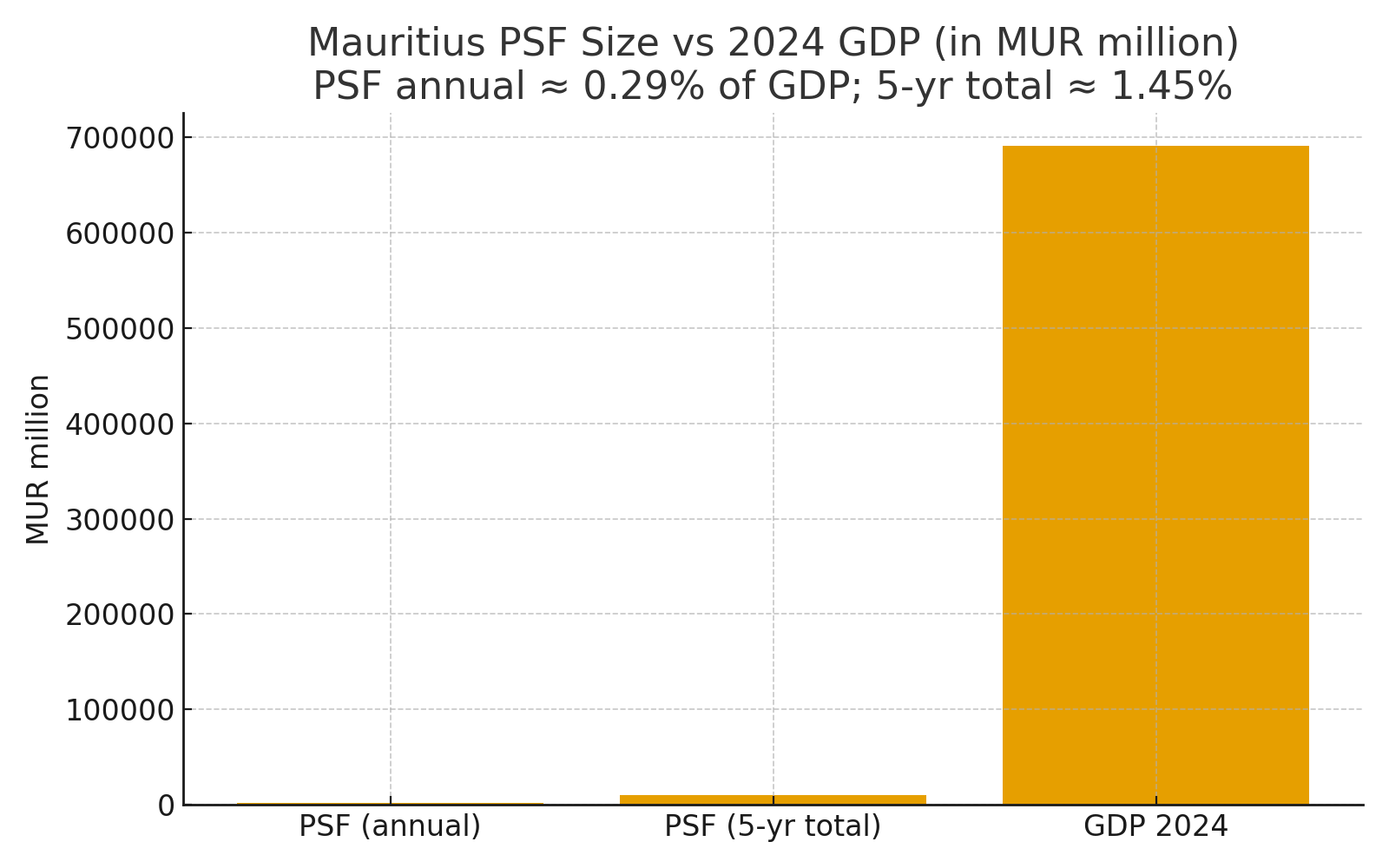

On 16 August 2025, the Mauritian government unveiled a package of subsidies and a Price Stabilization Fund (PSF) designed to cushion households against inflationary pressures. The plan commits Rs 10 billion over five years, with Rs 2 billion allocated annually, to cap the prices of key staples. Bread will remain fixed at Rs 2.60 — a move expected to cost around Rs 450 million each year — while subsidies on milk powder, edible oil, infant milk, baby diapers, and processed cheese are budgeted at Rs 400 million over six months.

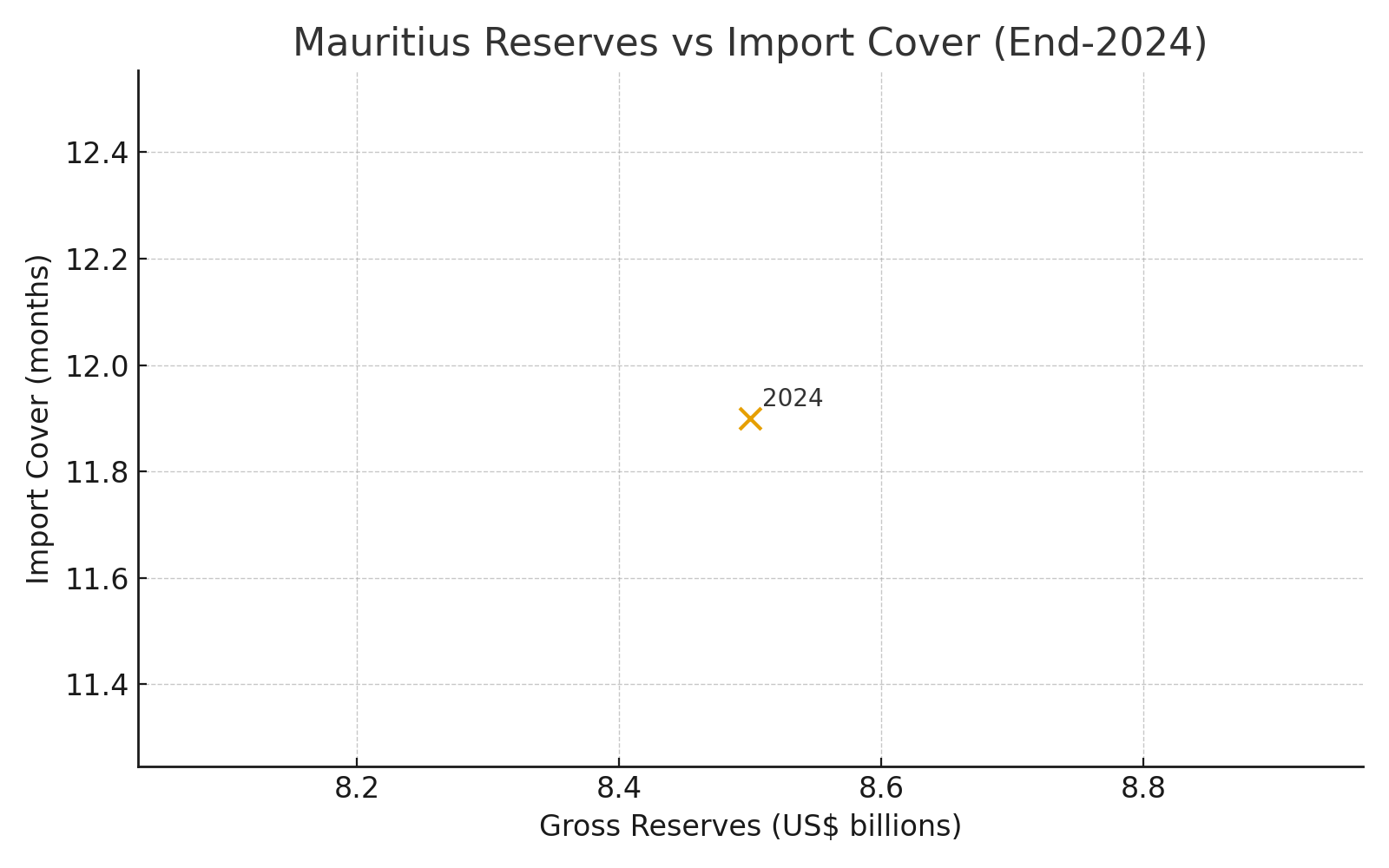

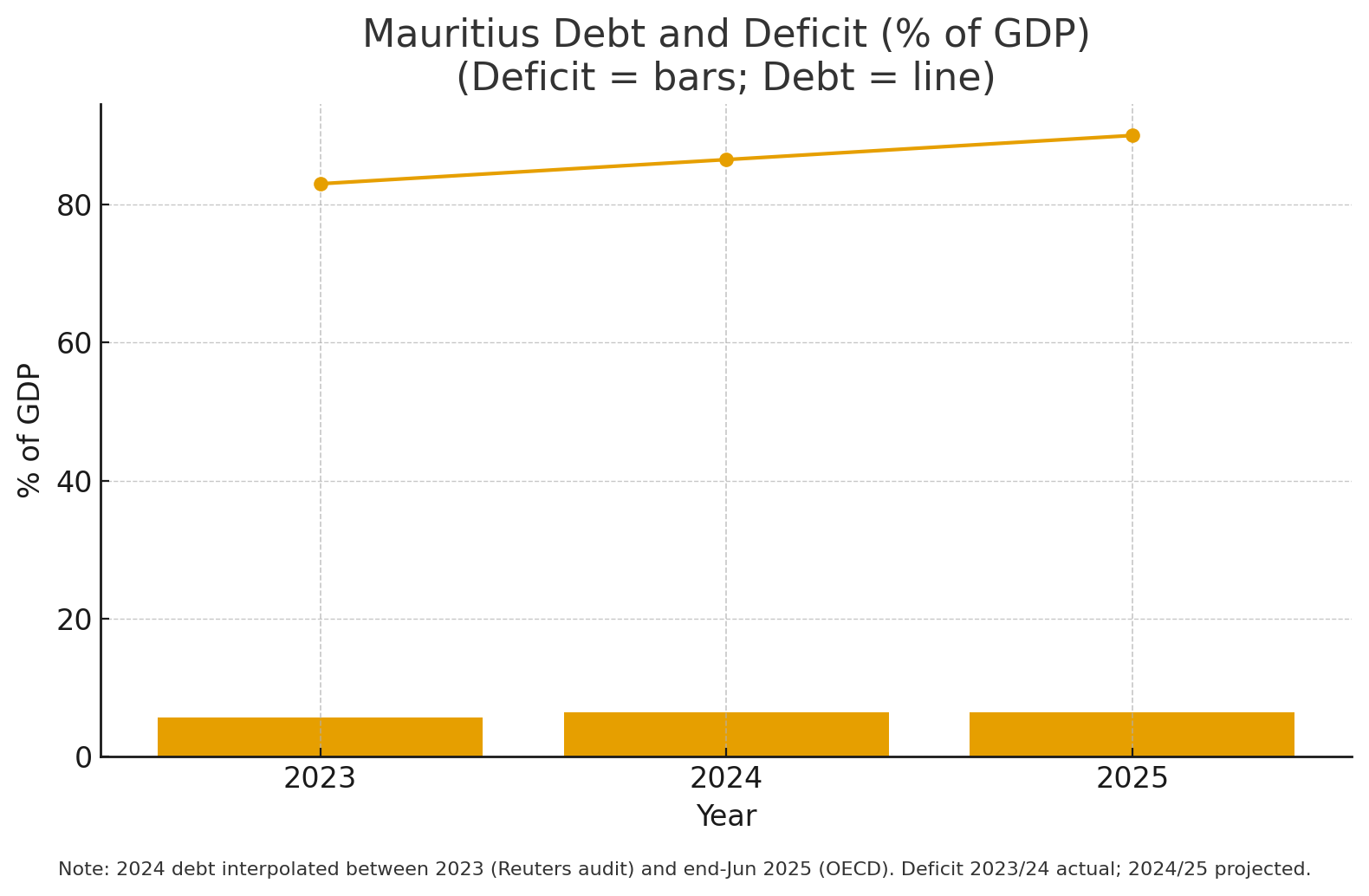

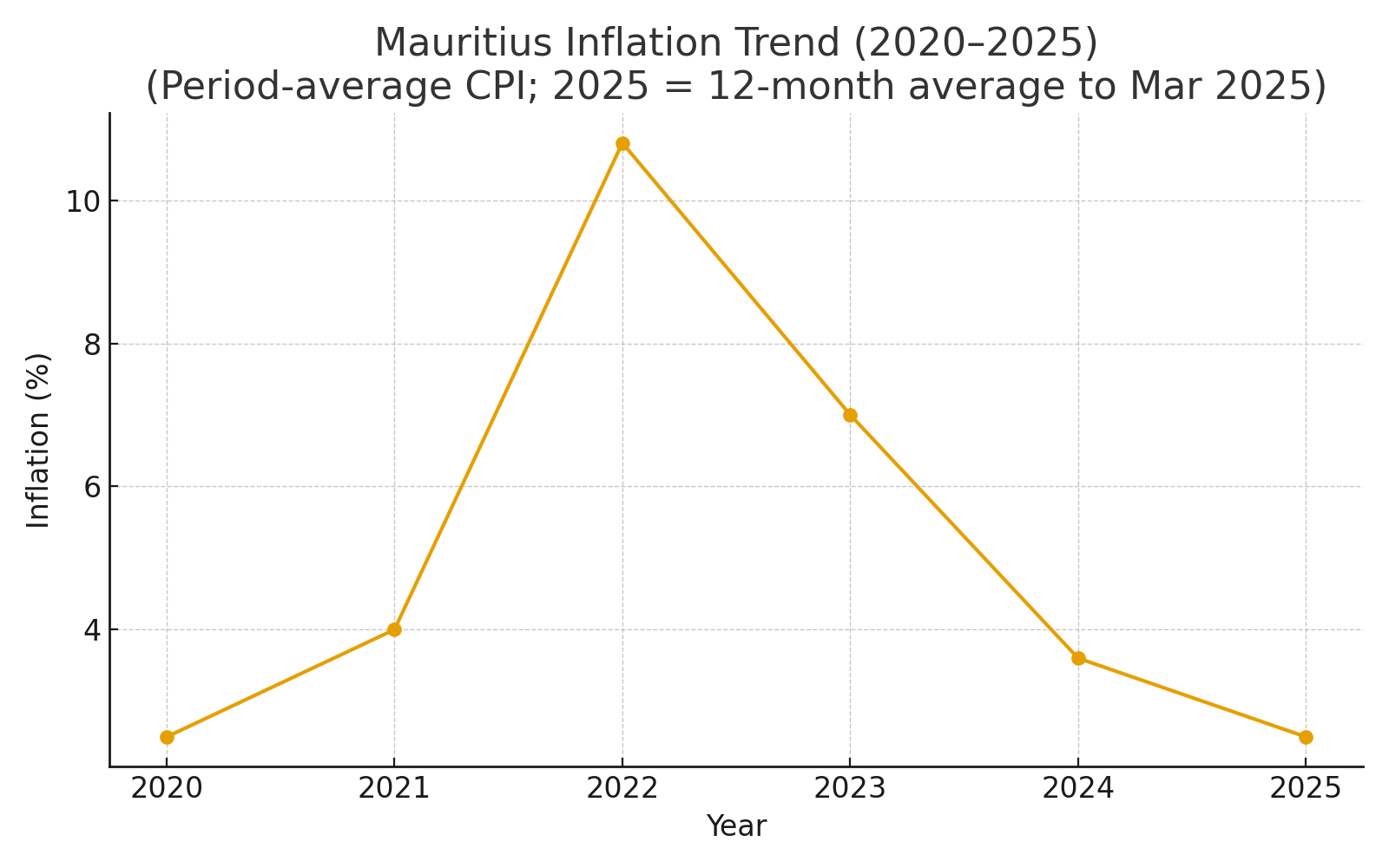

The decision comes at a time when the domestic economy shows signs of easing inflation but rising fiscal vulnerabilities. After peaking near 7% in 2023, headline inflation fell to 2.6% by mid-2025 (MUR inflation index). Growth has moderated, with real GDP expanding by 4.7% in 2024 but expected to slow to just above 3% in 2025, according to official forecasts. Public debt reached close to 90% of GDP by June 2025, and the budget deficit is projected at 6.4% of GDP for the 2024/25 fiscal year. Mauritius’ reserves — about USD 8.5 billion (MUR/USD FX: MUR=X) at end-2024, covering nearly 12 months of imports — provide some cushion, but not unlimited space.

These numbers illustrate the trade-off Mauritius faces. Subsidies are politically popular and provide tangible relief for households, but they come at a fiscal cost. Maintaining low consumer prices in a high-debt environment risks widening the deficit further, especially if subsidies extend beyond their intended duration. The government itself has acknowledged the potential strain on public finances and the risk of a credit rating downgrade if expenditure pressures persist.

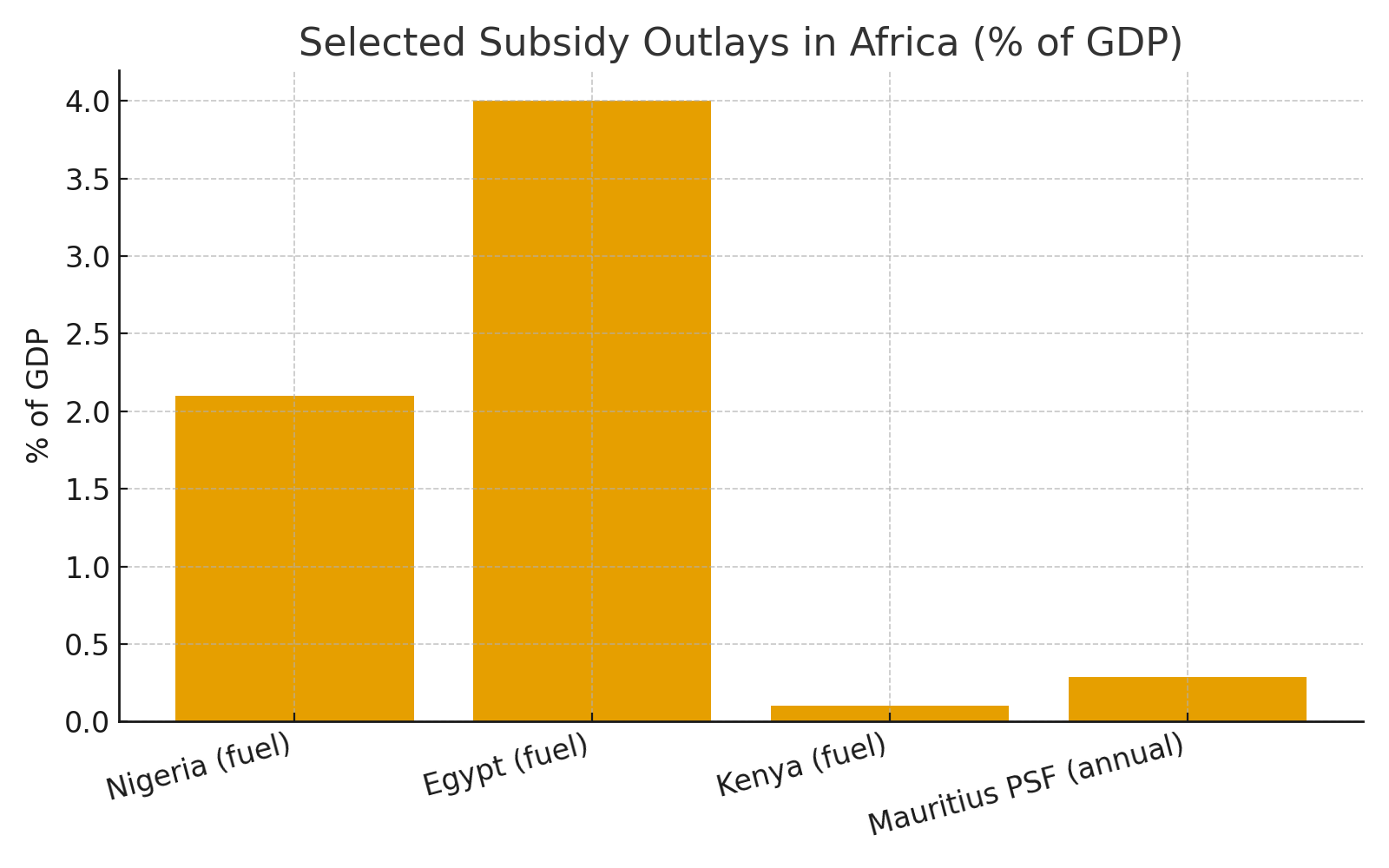

Comparisons with other economies across Africa show how widespread this dilemma has become. In Nigeria (NGN=X, NGERGGOV), the removal of fuel subsidies in 2023 saved billions of dollars but led to immediate social unrest. In Egypt (EGP=X, EGYGB 2032 Eurobond ISIN XS2107200273), subsidies on bread and fuel consume more than 6% of GDP, a level that constrains fiscal flexibility despite helping to maintain stability. In Kenya (KES=X, KENGOV 2031 ISIN XS2356566267), the government alternated between fuel and fertiliser subsidies, but rising debt and IMF programme conditions forced periodic rollbacks. Mauritius’ PSF, though smaller in scale, reflects the same underlying tension between short-term relief and long-term sustainability.

For investors, Mauritius’ subsidy programme is more than a domestic adjustment. The country is one of Africa’s few upper-middle-income economies, long positioned as a financial hub and gateway for investment flows. When an economy with such credibility commits Rs 10 billion to subsidies, it signals the depth of inflation’s political and social impact across Africa. Investors tracking African sovereign bonds (e.g. Mauritius 4.2% 2032 ISIN MU0GN0200008), exchange rates (MUR=X, USDZAR=X, USDNGN=X, USDEGP=X, USDKES=X), or regional equity benchmarks (Nairobi All Share NASI.IND, Egyptian EGX30 EGX30.CA, Nigerian NGX All Share NGSEINDX) see in Mauritius a test case of how even relatively stable economies must weigh fiscal prudence against household relief.

Analytical Charts

For Africa more broadly, the Mauritius episode is part of a continental story: the subsidy dilemma. Nigeria’s $10 billion fuel subsidy bill, Egypt’s subsidy spending above 6% of GDP, and Kenya’s stop-start subsidies all illustrate how governments are caught between stabilising societies and safeguarding fiscal health. Mauritius adds a new dimension: if a small, relatively diversified and well-managed island state struggles with this balance, then larger, more debt-burdened economies face an even sharper challenge. The policy choices Mauritius makes — whether it successfully tapers subsidies or slides into long-term commitments — will be closely watched as a signal of what is fiscally and politically possible across the continent.

This matters because global capital increasingly treats African economies as part of an interconnected risk pool. A subsidy-driven deficit in Mauritius could influence how investors price risk not only for Port Louis but for Lusaka, Nairobi, and Cairo. Conversely, a disciplined exit strategy could strengthen confidence that African governments can navigate inflationary shocks without sacrificing macroeconomic stability. In that sense, Mauritius’ bread price freeze is not a small domestic detail; it is a litmus test for Africa’s ability to deliver social protection without eroding investor trust.