China–Latin America Forum: Signals for Africa and Global Markets

China’s Wuxi forum with Latin America may seem modest — a USD 150m hub and a sugar deal — but it signals Beijing’s bid to reshape supply chains. Africa, the West, and investors must read it as a warning: adapt, compete, or risk irrelevance in the next trade era.

At the Eighth Dialogue between China and Latin America and the Caribbean Civilizations, held in Wuxi, Jiangsu, last week, Beijing unveiled a set of trade agreements that appear modest at first glance — a USD 150 million logistics hub, a one-million-ton sugar purchase, and a cross-border e-commerce pact. Yet behind the headlines lies a larger story: China is quietly redrawing the map of global supply chains. What state media presented as a routine South–South exchange was, in reality, part of a deliberate strategy to secure commodities, consolidate logistics, and extend influence into regions long considered within Western reach.

The timing of the forum is no coincidence. It comes as global growth slows, U.S.–China tensions sharpen, and the gap between developed and developing economies widens. Against this backdrop, Beijing is moving decisively to lock in commodity flows, build logistics anchors inside China, and promote “Chinese-style modernization” as a cooperative alternative to Western-led models. For Latin America, facing fiscal strain and volatile commodity markets, China offers both a stable buyer and a source of new capital — a partnership that appears transactional on the surface but carries deep strategic weight.

The deals themselves tell the story. The CIASA International Trade Hub, at USD 150 million, is small by Chinese standards but symbolically important. It establishes a one-stop platform in Wuxi for Latin American exporters, lowering barriers to entry into the Chinese market. The sugar procurement deal, equivalent to roughly five percent of Brazil’s 2024 exports, signals Beijing’s determination to guarantee food and commodity supplies at scale. The e-commerce memorandum promises to build joint procurement platforms and digital pipelines, potentially reshaping how Latin American goods flow to Chinese consumers. None of these projects alone will shift the global balance, but together they institutionalize new channels of trade that bind Latin America more tightly into China’s orbit.

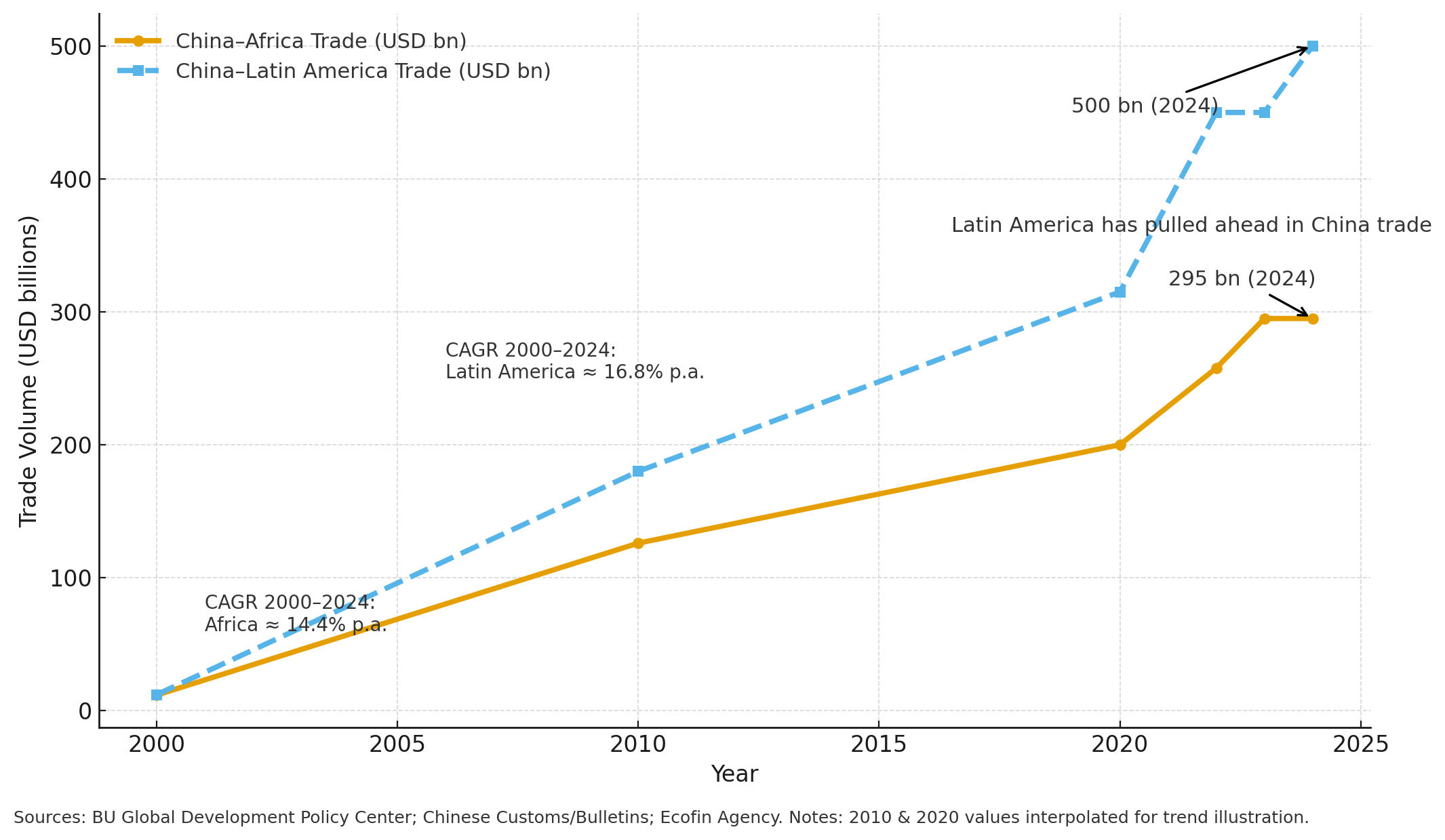

The economic implications are immediate. China–Latin America trade surpassed USD 500 billion in 2024, compared with USD 282 billion with Africa. Latin America is already outpacing Africa in capturing Chinese demand, particularly in agriculture. For African producers of sugar, coffee, or pulses, the competition is clear: Brazilian scale and reliability pose a challenge. Unless Africa leverages the African Continental Free Trade Area to negotiate collective access, it risks being sidelined. Wuxi shows how much advantage can be gained when logistics infrastructure is established inside China itself. Africa should be pressing for equivalent “Africa Trade Houses” in Chinese cities, not merely waiting for buyers to come.

Risks, however, loom large. Commodity markets are volatile, and locking in procurement contracts without adequate hedging can backfire. Latin America’s political cycles are notoriously turbulent; elections in Brazil, Argentina, or Mexico could quickly shift policy direction. Logistics hubs under the Belt and Road have often faced delays, cost overruns, or weak uptake, raising doubts about whether Wuxi’s promises will materialize. Overreliance on a single buyer also creates dependency, eroding long-term bargaining power. These vulnerabilities were absent from the official narrative but are precisely what investors and rival powers will be scrutinizing.

The implications extend beyond Africa and Latin America. In Washington, the symbolism of Latin America deepening ties with Beijing is viewed as a strategic incursion into America’s backyard. A logistics hub and sugar contract may look modest, but they are interpreted as China entrenching itself in a region where U.S. influence has historically been dominant. In Brussels, the worry is about supply chains: Europe is competing with China for agricultural commodities and green-energy inputs, and each deal signed in Wuxi reduces European access. In New York and London, analysts look past the politics to the market signals: one million tons of sugar is meaningful support for global prices, while a Chinese trade hub centralizes procurement under Beijing’s control. Just as significant is the currency dimension. If even a portion of these contracts are settled in renminbi, it is another incremental challenge to the dollar system — a trend Western financial strategists cannot ignore.

Markets will watch commodity-linked equities first. Brazilian sugar giants such as Raízen (RAIZ4.SA) and Cosan (CSAN3.SA) could see upside from guaranteed demand, while U.S.-listed agricultural traders like Bunge Global (BG) and Archer-Daniels-Midland (ADM) may need to reposition. On the Chinese side, logistics and e-commerce platforms including Alibaba (BABA), JD.com (JD), and Pinduoduo’s PDD Holdings (PDD) stand to gain from expanded cross-border flows. Global sugar futures (ICE: SB=F) already trade with tight supply margins, and a one-million-ton procurement adds bullish pressure.

The bond and currency markets will be no less responsive. Greater settlement in offshore renminbi (CNH) would shift hedging strategies across Latin America, just as the Brazilian real (BRL) and Mexican peso (MXN) are closely tracked by FX desks. For fixed income, Brazil’s 10-year government bond yield (BZ10Y) offers a barometer of how capital markets digest Chinese demand for commodities, while Mexico’s sovereign curve (MX10Y) may reflect the spillover. Broader emerging-market debt ETFs such as the iShares J.P. Morgan USD Emerging Markets Bond ETF (EMB) and the VanEck J.P. Morgan EM Local Currency Bond ETF (EMLC) give investors exposure to how renminbi-linked procurement shifts risk premia across the developing world. African sovereigns, particularly Ghana (GHANA 2032 USD bond) and Kenya (KENINT 2031), will be benchmarked against how Latin American credits perform under this new wave of Chinese financing.

What the West sees as risk, it also sees as opportunity. The fragility of commodity prices, the unpredictability of Latin American politics, and the execution gaps in Chinese infrastructure projects create openings for U.S. and European institutions to offer alternative financing, regulatory stability, or technology partnerships. Western policymakers will view Wuxi not simply as a trade event but as a signal that they must accelerate counter-offers such as the U.S. Partnership for Global Infrastructure and Investment or the EU’s Global Gateway.

For Africa, the lesson is sharper still. Latin America is turning its commodities into structured, long-term access deals. If Africa limits itself to raw material exports without demanding value-addition or collective bargaining power, it risks falling behind. Negotiating through AfCFTA gives the continent more leverage, but that leverage must be used to secure logistics access, technology transfer, and local processing — not just bulk exports.

For global markets, the Wuxi announcements serve as forward indicators. Commodity traders should expect China’s procurement to support prices in sugar, soy, and eventually metals. Sovereign wealth funds and central banks should anticipate greater use of the renminbi in trade settlements, shifting FX and reserve strategies. Equity investors will monitor logistics and e-commerce firms for growth, while fixed-income desks track EMB, EMLC, and sovereign spreads for signs of how Chinese engagement reprices risk across the Global South.

The Wuxi forum was not about sugar or cultural diplomacy. It was about power. China is reorganizing global commodity routes and setting the rules of tomorrow’s trade corridors. Africa must see it as a benchmark to demand stronger terms. Western capitals will view it as a competitive threat that requires a strategic counterweight. And for investors, it is an unmistakable signal of where Chinese demand, currency flows, and supply chain power are headed. Wuxi is a mirror — and the question for the rest of the world is whether to adapt, compete, or risk irrelevance.