Central Bank of Ghana Slashes Monetary Policy Rate from 25% to 21.5%.

BoG’s second jumbo cut—350 bps to 21.5%—signals a shift from crisis control to disciplined easing. With inflation at 11.5%, real rates stay tight, bills should rally, the cedi looks steadier on stronger reserves, and banks’ funding costs fall. Risks: tariffs, commodity swings, over-easing bets Ahead

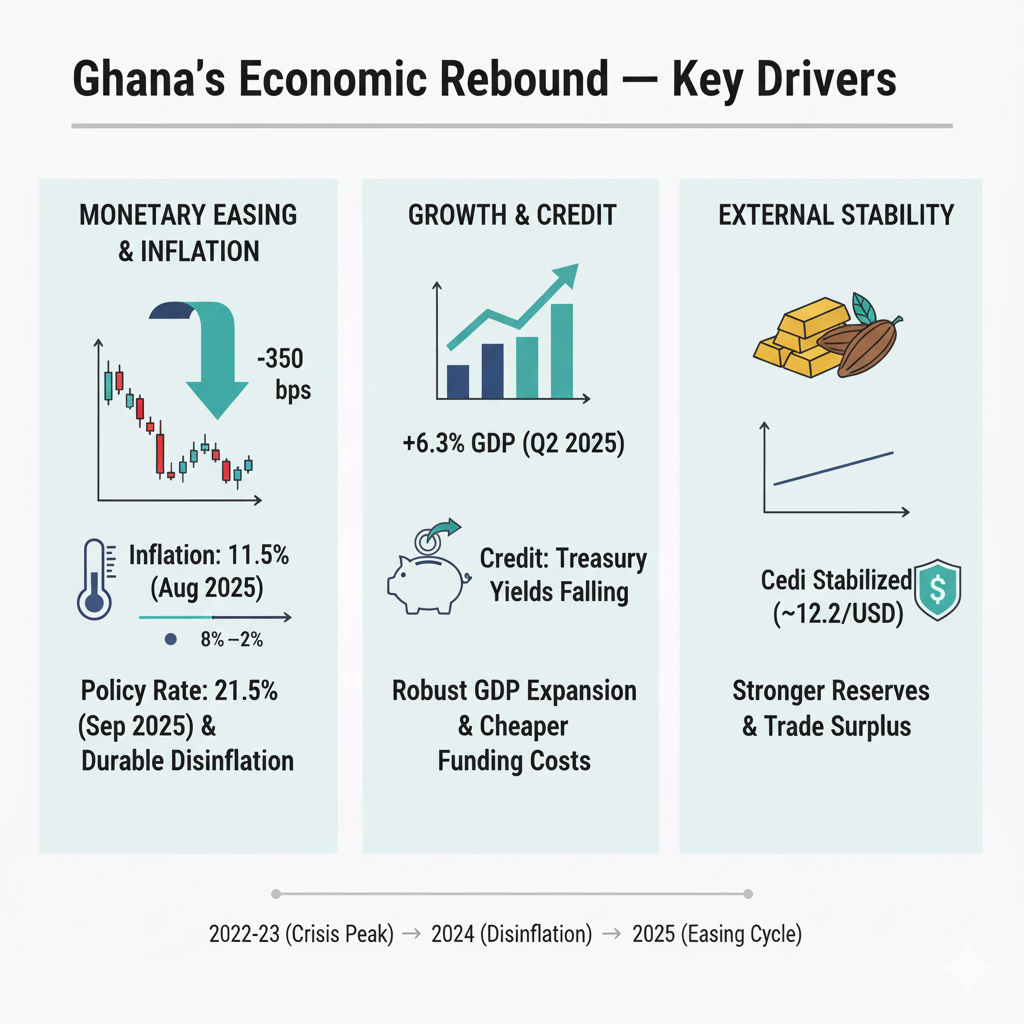

Ghana’s Monetary Policy Committee has shifted decisively into easing mode, cutting the policy rate by 350 basis points to 21.5% after July’s 300-point move—650 bps of reductions year-to-date. The logic is straightforward: disinflation looks durable, external buffers are stronger, and even after the cut the stance is still restrictive. With headline inflation down to 11.5% in August—the lowest since late 2021—and guidance that price growth should settle in the 8% ±2 band by year-end, the ex-post real policy rate still sits near +10%. That gives the Bank of Ghana room to ease the brake on credit without abandoning its anti-inflation posture.

Transmission is already showing up where it bites first: the Treasury front end. At the latest auction, interest-equivalent yields printed around 10.53% on the 91-day, 12.44% on the 182-day, and 12.96% on the 364-day—well below the policy rate and steadily compressing since mid-year. That is classic early-cycle behavior, signaling improving liquidity and policy credibility. If incoming CPI releases keep trending toward target, front-end bills should continue to grind lower, anchoring funding costs for banks and corporates. On screens, track GH91D, GH182D, and GH364D for confirmation.

Growth no longer looks like the constraint it was during the 2022–23 stress. Real GDP rose 6.3% year-on-year in the second quarter of 2025, driven by a strong services rebound and non-oil GDP up 7.8%. That composition matters: broad, domestically driven growth reduces the risk of demand-pull inflation as borrowing costs fall, giving the MPC space to front-load normalization while keeping real rates positive. For a quick macro pulse, the GSS GDP series is the label most desks use.

The external account is the real regime change. Gross international reserves are about US$10.7 billion—roughly four and a half months of import cover—while the year-to-date trade surplus has widened to roughly US$6.2 billion, supported by gold receipts and a partial normalization in cocoa flows. In the interbank market, the cedi has stabilized around GHS 12.1–12.3 per USD with a meaningful year-to-date appreciation. Bigger buffers and a narrower external funding gap lower the risk that easier policy spills into FX disorder. Terms-of-trade drivers to watch are XAUUSD (gold) and CC=F (cocoa), while spot and interbank quotes will show up as USDGHS or USDGHS=X.

Taken together, the decision looks less like a gamble and more like a data-led recalibration. The policy path over two years tells the story: a peak at 30% in 2023 to arrest the inflation-FX spiral; a trim to 27% by September 2024 as disinflation gained traction; a precautionary nudge to 28% in March 2025 while waiting for confirmation; then a 300-bp move in July and 350-bp in September to 21.5% as the glidepath firmed. The stance has moved from crisis containment to restrictive normalization—still tight in real terms, but no longer choking credit.

For markets, the implications are clear without shouting them in bullets. The front end of the curve should remain on a downward trajectory if CPI cools and auction cover stays healthy; occasional re-steepening in the 6–12-month sector is likely as investors handicap the pace of subsequent cuts. In FX, the base case is stability to slight firming so long as reserves build and the trade surplus holds; watch USDGHS alongside XAUUSD and CC=F for direction. Banks should see funding costs drift down as time-deposit and bill rates reset, with lending rates following more slowly; net-interest margins may compress at the edges, but rising loan volumes and improving asset quality can offset the squeeze—use the Ghana Reference Rate (GRR) and monthly lending-rate/NPL prints as lead indicators. On equities, rate-sensitives—banks like GCB.GH and CAL.GH, consumer names such as MTNGH.GH, and housing-adjacent plays—typically lead early in easing cycles as discount rates fall and real incomes recover; the broad tape is GSE-CI. In external debt, spreads bias tighter if disinflation persists and reserve metrics hold, though global rates remain the spoiler; traders will quote GHANA 29s/32s/35s by maturity bucket.

None of this is risk-free. An administered-price shock from utilities would slow the descent toward the target band and stall the front-end rally, visible first in GH91D and GH182D. A terms-of-trade wobble in cocoa or gold would test the trade surplus and reserve trajectory, likely showing up as upward pressure on USDGHS. And if markets race ahead and price an overly rapid easing path, expect guidance to lean against an unhelpful bull-steepening.

Bottom line: the cut to 21.5% makes macro sense and is market-positive. With a still-restrictive real rate, falling inflation, firmer reserves, and a steadier currency, the baseline is lower bill yields (GH91D/GH182D/GH364D), stable USDGHS, gradually easier credit via the GRR channel, and selective opportunities to add duration—so long as the inflation glidepath and external buffers remain intact.