Can Zambia Leapfrog Chile and Peru? Kansanshi’s Expansion Tests Global Markets

First Quantum (TSX: FM) is betting $1.25B on Kansanshi’s S3 to replace lost Panama output and anchor Zambia’s 3 Mt copper goal. Success could reprice Zambia’s Eurobonds and shift global supply chains, but execution and policy risks loom.

Zambia’s copper narrative has entered a new phase with the USD 1.25 billion Kansanshi S3 expansion, a project that promises to extend the life of one of Africa’s largest mines into the 2040s and push output significantly higher. Kansanshi, owned 80% by First Quantum Minerals (TSX: FM) and 20% by state vehicle ZCCM-IH (LUSE: ZCCM), produced around 171,000 tonnes of copper in 2024. With the S3 expansion, annual output could rise toward 250,000 tonnes, adding scale at a time when Zambia is targeting a national production goal of 3 million tonnes of copper per year. For global investors, this is more than a local mining story: it is a potential re-rating of Zambia as a critical supply node in the global copper chain.

The S3 expansion comes as First Quantum (TSX: FM) reels from losing its Cobre Panamá mine, making Zambia its anchor asset in both output and valuation. Beyond boosting volumes, the project aims to modernize processing and cut costs, keeping Kansanshi competitive on the global curve. To fund its Zambian push and repair its balance sheet, First Quantum has flagged capital reallocation and possible stake sales, with reports of Saudi interest via Manara Minerals. For Zambia, S3 and other mine expansions are a chance to restore lost momentum. Hitting a 3 Mt copper target would place the country among the world’s top three producers, strengthening the kwacha, lifting fiscal revenues, and potentially easing sovereign risk. With copper already over 70% of export earnings, any step-change in output could improve Eurobond sentiment and narrow the sovereign risk premium.

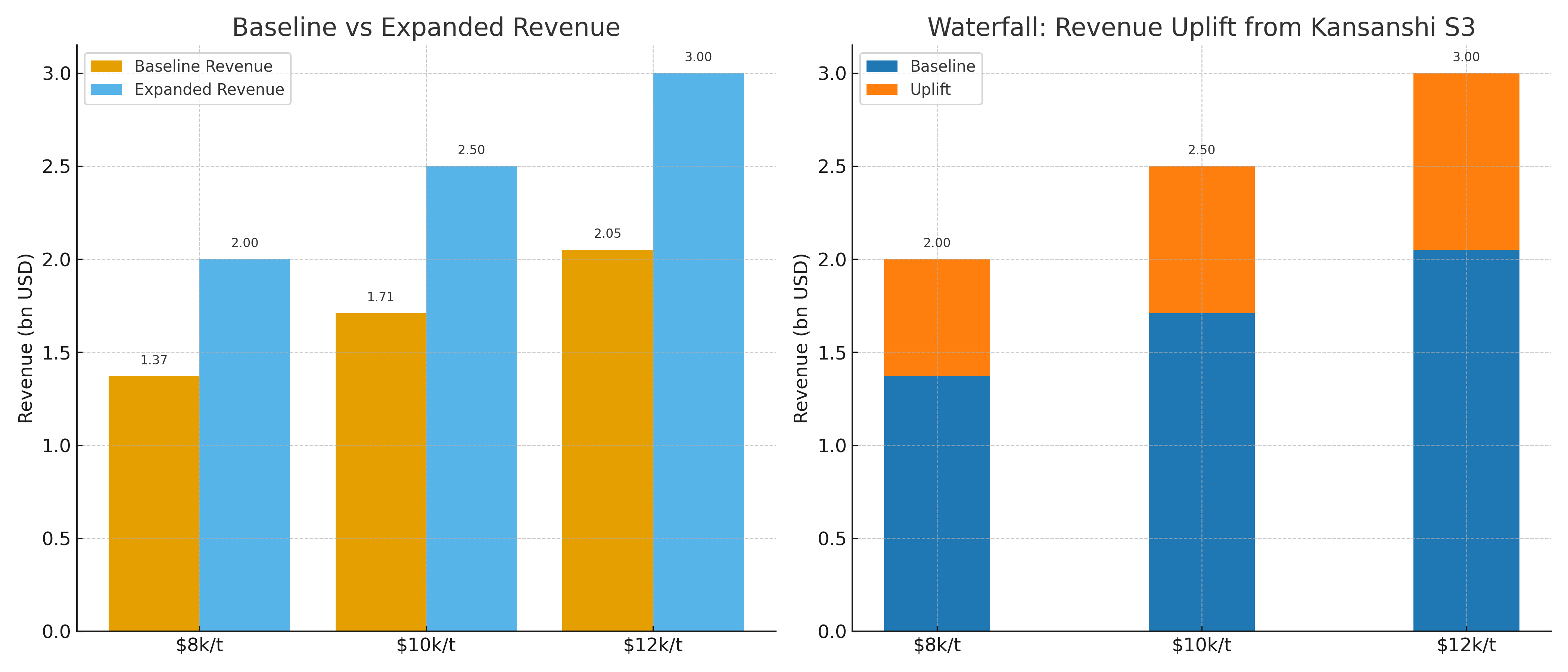

Kansanshi S3 – Copper Price Scenarios & Revenue Uplift

Illustrative model using baseline 171,000 t vs expanded 250,000 t. EBITDA margin assumed 40%; royalty at 10% band for high prices.

| Scenario | Copper Price (USD/t) | Baseline Revenue (bn USD) | Expanded Revenue (bn USD) | Revenue Uplift (bn USD) | % Uplift | EBITDA Uplift (bn USD) | Govt Royalty @10% (bn USD) |

|---|---|---|---|---|---|---|---|

| $8k/t | 8,000 | 1.37 | 2.00 | 0.63 | 46.2% | 0.25 | 0.06 |

| $10k/t | 10,000 | 1.71 | 2.50 | 0.79 | 46.2% | 0.32 | 0.08 |

| $12k/t | 12,000 | 2.05 | 3.00 | 0.95 | 46.2% | 0.38 | 0.09 |

From a global markets lens, Kansanshi’s value lies in shifting supply-demand. With structural copper deficits expected from 2026, Zambia’s ramp-up could temper short-term spikes, diversify supply away from politically fragile Chile and Peru, and serve as a hedge for Asian and European buyers. Risks remain: execution challenges, cost overruns, policy shifts, and First Quantum’s debt load all weigh heavily. For investors, Zambian copper offers portfolio upside in a high-demand metal but comes with sovereign and operational volatility.

For equity markets, the trade is two-fold. First Quantum Minerals (TSX: FM) could see re-rating if S3 is delivered on time and at cost, providing clarity after the Panama setback. ZCCM-IH (LUSE: ZCCM) as the minority partner could capture dividends and capital appreciation if revenues rise, giving local investors a leveraged play. Globally, copper majors like Glencore (LSE: GLEN), BHP (ASX: BHP), and Rio Tinto (LSE: RIO) will monitor Zambia’s progress, as increased competition for resource nationalism deals or partnerships may shift the landscape. Traders such as Trafigura and Chinese state buyers may also tighten offtake arrangements to secure long-term supply.

Fixed-income investors should view Kansanshi’s expansion as part of Zambia’s sovereign credit story. Eurobonds, long under restructuring pressure, could benefit if copper revenues stabilize external balances. Ratings agencies will demand execution, but credible progress toward 3 Mt strengthens the case for narrowing spreads against regional peers. For long-horizon investors, the S3 project signals Africa’s growing role in the energy transition. Copper is vital to electrification, and expansions in low-cost, long-life assets within stable jurisdictions will attract premium valuations.

Zambia’s test is to turn this into a durable, predictable mining policy that reassures capital. The bottom line: with USD 1.25 billion committed, Kansanshi repositions Zambia on the global copper map, with consequences for prices, credit, equity, and strategic flows. For First Quantum, it is an execution trial; for Zambia, a chance to turn geology into fiscal strength; and for global markets, a reminder that frontier assets can suddenly become central to supply chains.