Can IWY Sustain AI-Led Growth? What Investors Should Know

The iShares Russell Top 200 Growth ETF (IWY) appears diversified but is dominated by mega-cap tech, creating an illusion of breadth. It thrives in AI-led booms yet suffers sharper losses in downturns. IWY is best treated as a tactical satellite bet, not a core portfolio holding.

In the current market cycle, few themes dominate investor narratives as much as artificial intelligence. ETFs such as the iShares Russell Top 200 Growth ETF (IWY) appear, at first glance, to offer broad exposure to this growth story. With more than one hundred holdings, IWY carries the branding of a diversified vehicle. Yet beneath the surface, the numbers tell a very different story.

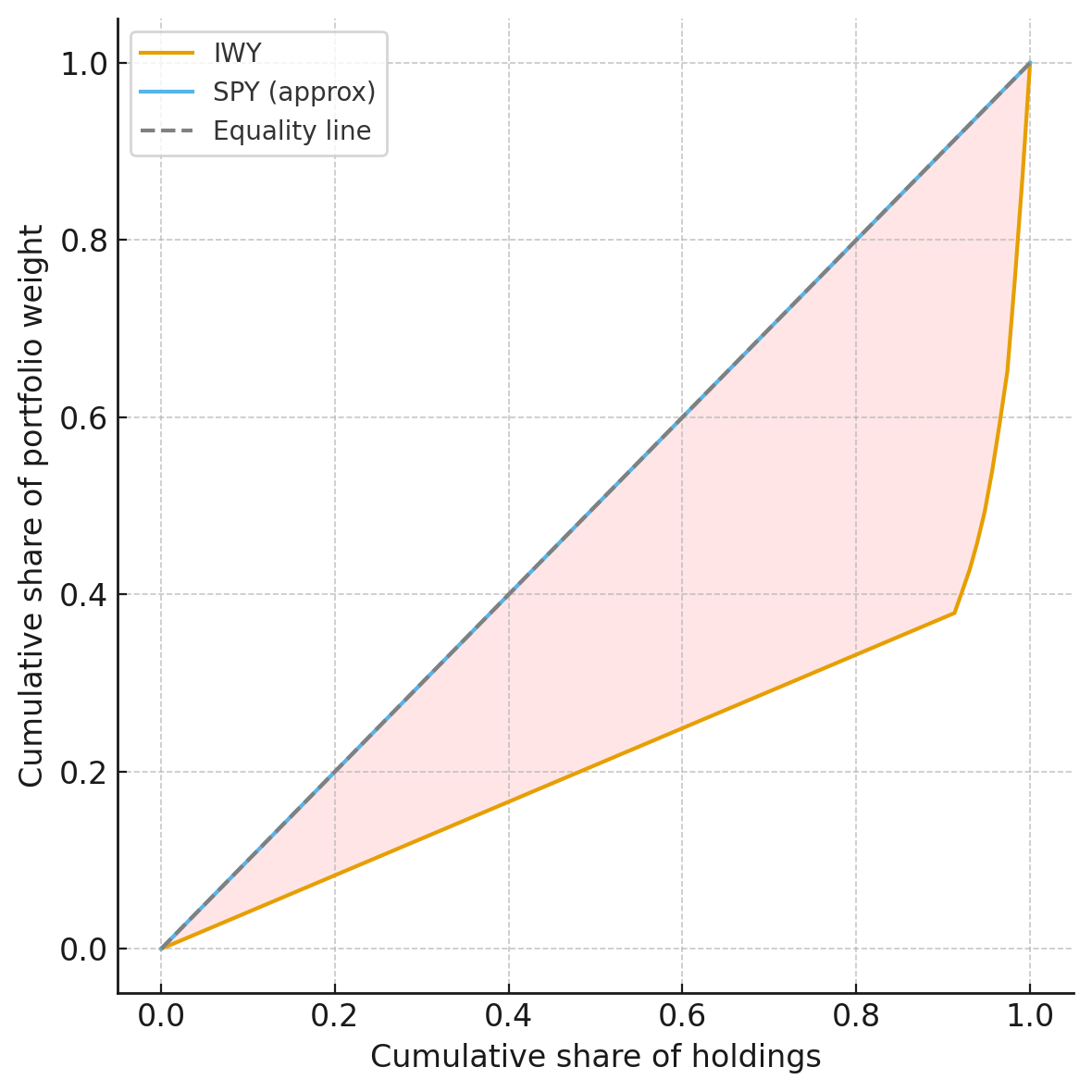

An empirical look at the fund reveals that IWY’s top ten holdings, led by NVIDIA, Microsoft, and Apple, account for more than 62 percent of its total weight. Measures of concentration—such as the Herfindahl–Hirschman Index and the Gini coefficient—confirm that the fund’s effective diversification is closer to nineteen holdings, not one hundred. In practice, IWY behaves less like a broad growth ETF and more like a concentrated bet on a handful of mega-cap technology firms.

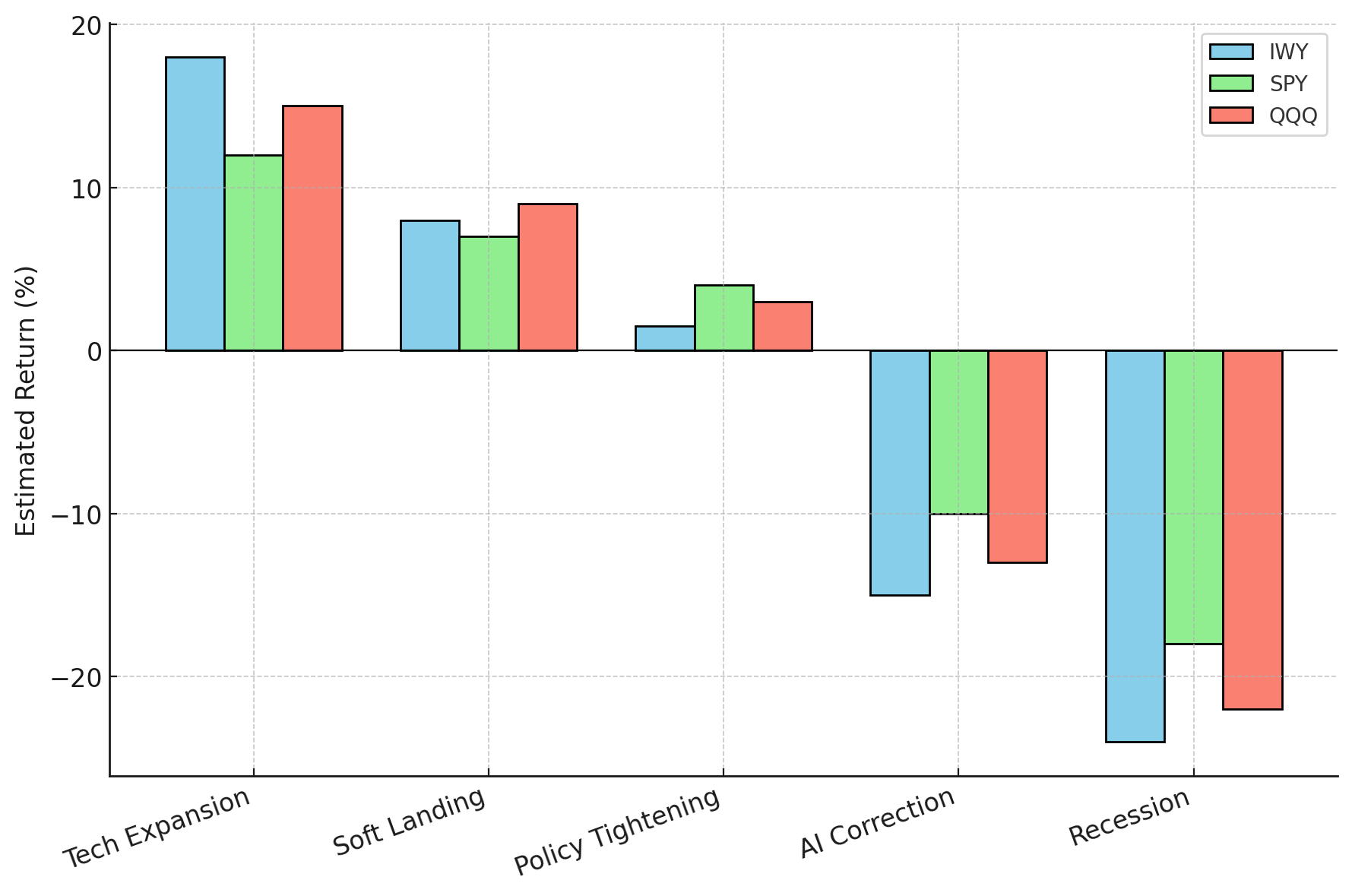

This concentration produces an asymmetric risk–return profile. In scenarios of rapid AI adoption and technology-led expansion, IWY delivers outsized gains, comfortably outpacing benchmarks like the S&P 500 and Nasdaq-100. But when the cycle turns—whether through sectoral overinvestment or a macroeconomic recession—IWY’s drawdowns deepen disproportionately, often exceeding 20 percent. Rather than smoothing risk, the ETF amplifies volatility, functioning almost like a leveraged option on the AI trade.

Adding to this vulnerability is IWY’s duration sensitivity. Growth stocks are long-duration assets, their valuations heavily dependent on future earnings. As such, they are particularly sensitive to changes in interest rates. The analysis shows that even with double-digit earnings growth, a modest rise in discount rates can wipe out performance gains through multiple compression. For investors, this means IWY’s fate is tied not only to the trajectory of earnings but also to the Federal Reserve’s monetary policy stance.

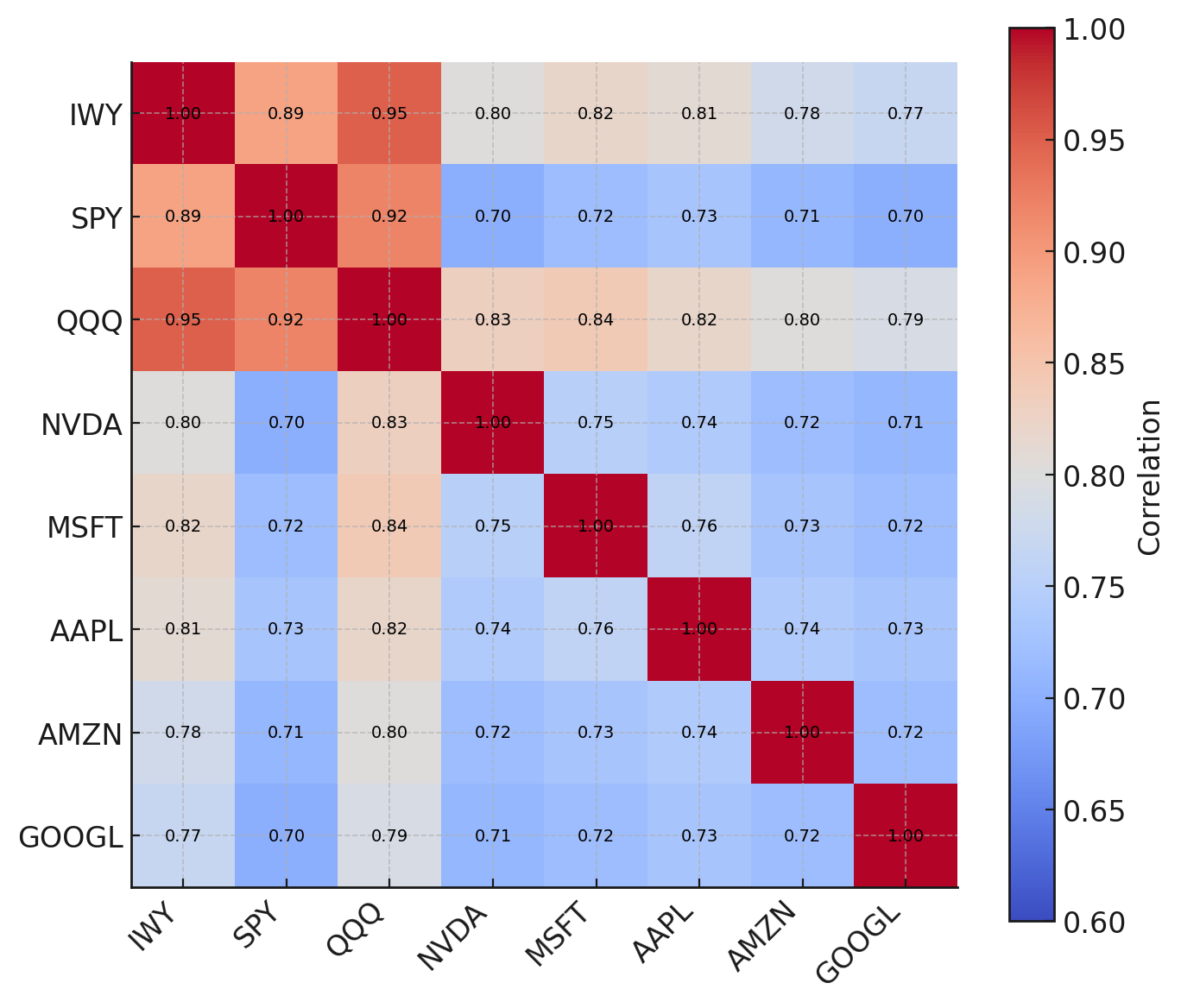

Policy risk compounds the challenge. At the macro level, IWY is exposed to monetary tightening, fiscal policy shifts in industrial subsidies, and geopolitical disruptions in semiconductor supply chains. At the micro level, its largest constituents face sustained antitrust scrutiny, the introduction of global minimum corporate taxes, and escalating ESG disclosure requirements. A regulatory shock to just one of its dominant holdings could reverberate across the ETF, given the high correlations among its top names.

For investors, the implications are clear. IWY should not be mistaken for a core portfolio holding. Instead, it is best deployed as a satellite allocation—a tactical instrument to capture upside in periods of AI optimism, but one that requires active risk management and hedging against downside risks. Holding IWY alongside QQQ adds little incremental diversification; it simply doubles down on the same concentrated exposures. Effective use of IWY means treating it as a targeted overlay, not as a substitute for broad growth exposure.

Portfolio managers, meanwhile, should provide greater transparency by reporting effective diversification metrics—such as HHI or effective number of holdings—rather than headline counts that obscure concentration. Regulators, too, may need to consider how passive vehicles like IWY transmit sector-specific risks into household portfolios, especially as retail capital continues to flow into index-linked products.

For academics and researchers, IWY offers a revealing case study in how innovation cycles intersect with financial structures. It shows how market-cap weighting can transform broad indices into concentrated vehicles and how policy shocks transmit through ETFs into systemic risk.

Ultimately, IWY embodies the paradox of modern indexation. Marketed as a broad growth vehicle, it is in reality a concentrated play on mega-cap technology—a fund that magnifies both the promise of AI-driven expansion and the perils of policy tightening, regulatory intervention, and sectoral overreach. For investors and policymakers alike, the lesson is clear: what looks diversified on paper may be far more fragile in practice.